Applying the IPCA model in the Brazilian market

Author: Helder Parra Palaro

Bayes Capital Management

The traditional methods of asset pricing consider risk factors as observable. The assets are sorted based on the risk factors, and alpha and betas are estimated by regression.

Alternatively, risk factors can be considered as latent, and estimated by principal component analysis. The main drawback of this approach is that it allows only the static estimation of the betas. Besides that, the method does not handle other information besides the panel of returns.

The IPCA model (Kelly, B., Pruitt, S. and Y. Su (2019) is a new method which maintain the advantages of the two approaches mentioned above. The risk factors are considered latent (non-observable). This avoids the necessity of establishing a priori which risk factors are important. All company characteristics (such as price/earnings, price/book, etc) are used as instrumental variables in the betas estimation, and these betas are dynamically updated. The asset expected returns still depend on risk factors and betas, as in the traditional asset pricing models, but these risk factors do not need to be specified a priori.

We estimated the IPCA model for the Brazilian market. Our data set contains 170 stocks, in the period from January/2002 to August/2020. Besides the asset returns, we have 112 company characteristics (price/earnings, volatility, price/book, etc). Following the authors, we considered 5 latent risk factors. We start with a window of 31 months, and re-estimated the model monthly expanding the window. The estimation method used is the Alternate Least Squares (ALS). Each month we estimate the betas and latent risk factors, and we propagate the betas for the next month. This way, we have predicted expected return for our assets in our portfolio. We create a long-only portfolio by choosing in each month the stock subgroup where the expected return is in the top quartile. We can finally calculate an out-of-sample return series .

Our benchmark is obtained using the traditional portfolio construction method for risk factor. We consider five family of factors: value, momentum, growth, low volatility and quality. We create five long-only portfolios, one for each of these families. We then use equal weights to combine these five portfolios in the final long-only portfolio.

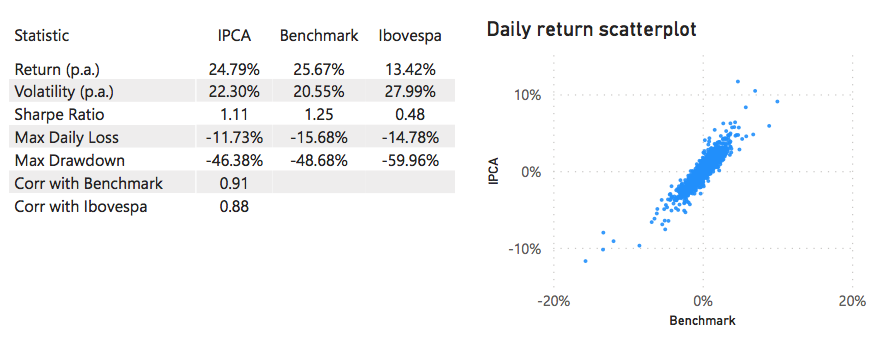

We list below the results obtained from August/2004 to August/2020.

For our dataset, the IPCA model does not outperform the traditional method, but the results are similar (Sharpe Ratio of 1.11 and 1.25, respectively. The maximum daily loss and maximum drawdown are reduced, which can be seen also in the left part of the scatterplot above. The 0.91 correlation show that although the models are similar, they obtain the results by different approaches.

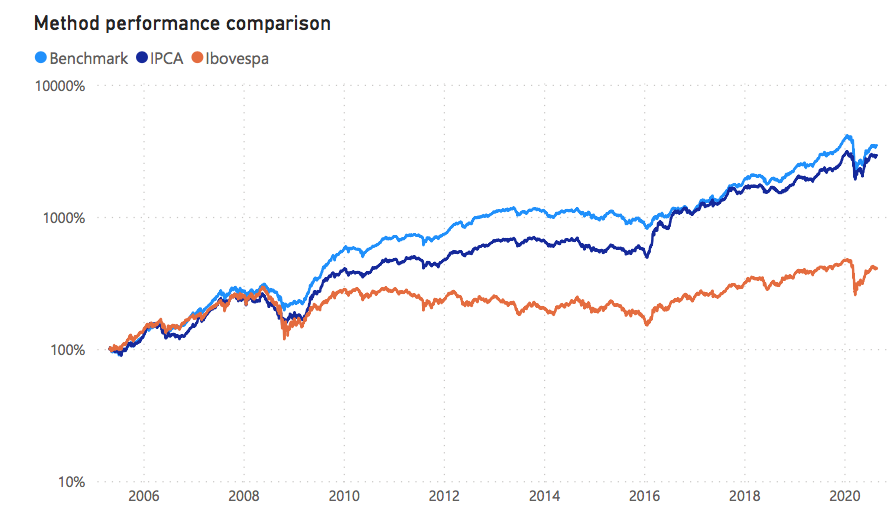

Given all above, the IPCA model is a method which considers the company characteristics as instrumental variables in the dynamic beta estimation and latent risk factors. In a portfolio of 170 Brazilian stocks in a 16-year period, the method slightly underperforms the traditional method of portfolio construction for risk factors, but with smaller losses in the distribution tail. We need also to consider that there is a possibility of overestimation of the performance of the traditional method, since all risk factors used to build the portfolio are well known in the finance literature.

Reference

- Kelly, B., Pruitt, S. and Su, Y., (2019). “Characteristics are covariance: a unified model of risk and return”, Journal of Financial Economics, 134 (3), 501-524.